The change in the price of input alters the cost of production of a commodity.

Let us analyze the two different cases.

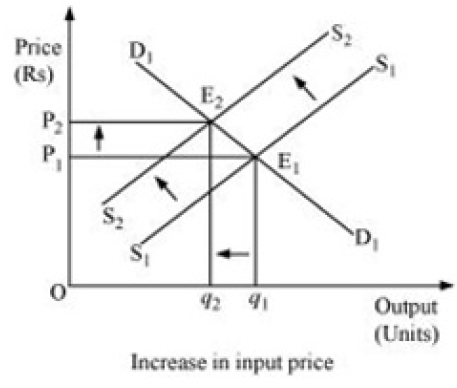

(a) Increase in input price: If the input price of a firm increases, the cost of production will also increase,the supply of product will decrease and the profit margin will also fall which will discourage the firm' incentive to produce and supply the commodity. This will lead to a left upward shift of the marginal cost curve, which further will lead to a leftward parallel shift of an individual firm' supply curve and finally a leftward shift of the market supply curve. The demand curve remaining the same, the new equilibrium will occur at E2 with higher equilibrium price (P2) and lower quantity of output (q2).

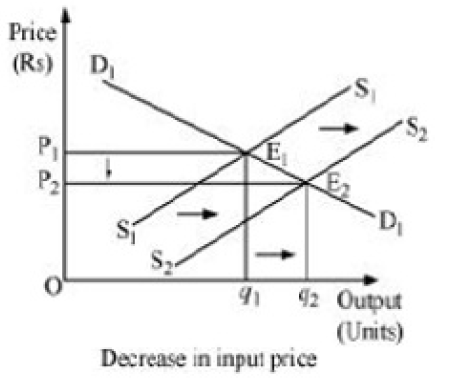

(b) Decrease in input price: If an input price of a firm decreases, then the cost of production will decrease, the supply of product will increase and the profit margin wll also rise. This will shift the marginal cost curve rightward, which implies that the firm'* supply curve will also shift rightward. Consequently, the market supply curve will shift rightward parallelly from S1S1 to S2S2. Demand curve remaining the same, the new equilibrium will occur at E2 with lower equilibrium price (P2) and higher quantity level of output (q2).